FORT Fencing

Agricultural & Equine Fencing

10 January 2026

Happy New Year! Christmas seems a long way back already, as 2026 gets off to a galloping start. Thankfully we seem to be hearing more positive news from our Customers this year than we were in the second half of 2025.

There’s still plenty of reporting around the dire state of construction activity and we’re clearly a long way off anything close to a buoyant market, but it does seem better.

The weather thus far has been very mixed, with some extremes. Great building days, backed up with awful storms and torrential rain, which makes it hard to plan or schedule works on site and this will impact demand for a while.

This newsletter originally started back when product availability was extremely difficult, around 2021. Since then of course, everything has changed and currently product availability is good, but we know that the underlying demand for price increases is lurking in the wings; manufacturers are struggling to make money.

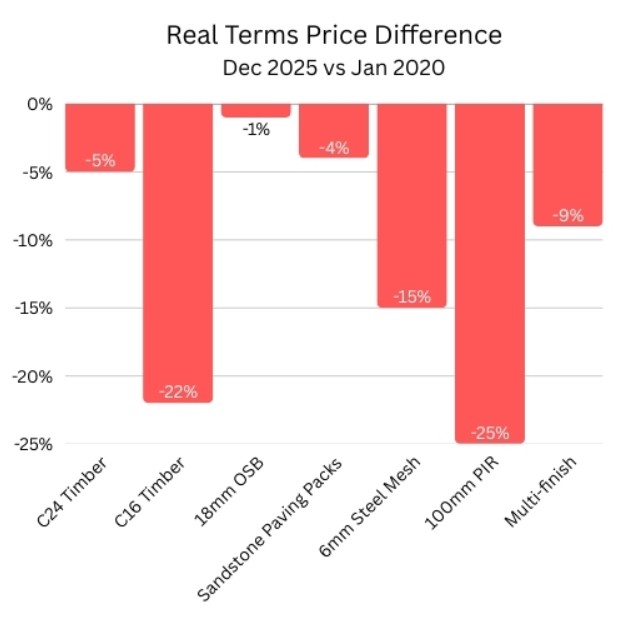

It seems like a good time to bust a few myths. Because we saw massive price inflation during COVID, the perception is that building materials are expensive, when that’s not actually the case. Here’s a few examples, based on the difference compared to general inflation:

Inevitably some have increased beyond inflation (cement for example), but the vast majority are lower.

So, you can explain to your Clients that now is actually a great time to build; they should be thinking about getting their project done now, before material prices begin to rise again.

As we show in our usual round up, interest rates have fallen (and might go further). This could be the ideal time to get the job done!

Our team came back from the Christmas break wonderfully rested and showing off their Christmas haul of new pants and socks, all eager to get back to work. Getting back up to speed was made more fun by the “variable” weather, with snow, torrential rain and unseasonably warm sunny days thrown in!

The beginning of January always feels like time for a bit of reflection of the year that’s passed and planning for the year ahead, and this month saw FORT’s 6th birthday which gave further cause for celebration. Amazingly the staff had room for some cake, and party spirit…

There are a wide range of price increase notifications coming through, so as always:Please wherever possible price ahead of time and build contingency for price increases into tenders for the future.

We mitigate price increases wherever possible, but we are seeing increases come through from our suppliers on a range of materials which look like they will stick. On the other hand, some material prices are reducing, meaning that we can pass on price decreases.

Key changes for February that have been advised from some suppliers of:

We will always do our utmost to defer or reduce the increases being imposed by the suppliers, and we have the power of the buying group that we are in to support that fight.

The FORT purchasing team are doing a great job of ensuring that we have stock on the ground and available at the right price, but as always, please forward-plan your requirement so that you aren’t caught short.

Here’s our round up of data to help you track key indicators that affect all of us:

Timber

This is a chart for the US market. As you can see it had been a huge roller-coaster, but has now been quite subdued for some time. This seems to show that the real US economy isn’t as positive as what their government seems to be portraying. The European market remains dull but availability is tight; low demand is holding back any increases. Current rates are still unviable in the medium term and are bound to rise at some point; we just don’t know when!

Weather & Climate - The overall rainfall trend is returning to normal after an extremely wet 2024. April 32%, May 56%, June 49%, July 90% August 50%, September 50%, October 75%, November 79% & December 87% of average rainfall. January has been very wet.

Currency - The £ has risen slightly against the $ (around $1.34 = £1) and this affects many items bought in $. The Euro has also weakened a little at around E1.15 = £1. The Swedish Krown (which affects timber) has stabilised at around Kr 12.40 = £1, from a previous range closer to Kr 13.80. That is now ‘baked in’ and timber prices from Sweden are adjusting accordingly. This will come through in due course as higher prices. As the largest producer of softwood, Sweden is very influential.

Oil Prices - These have such an impact on costs; despite the Middle East & Venezuelan situations, oil prices remain surprisingly stable at around $62 whereas they were around $77 a year ago. That means we’re currently tracking at prices well below the rate pre-invasion of Ukraine. It is unlikely to fall much further, so it could possibly be an inflationary concern.

Containers - There has been a fairly big increase in rates since December, but in overall terms they are still well below January 2025. This affects goods from India (sandstone) and the Far East (plywood for example). It is an important indicator. The US tariff battle with China caused disruption but the market seems to have adjusted.

Steel - Steel rates seem to be very settledand haven’t really moved in the last year. A rough balance between supply and demand seems to be in place.

Inflation/Interest Rates - This is the RPI figure and it fell to 2.7% in September but has come back to around 3.8%. This is a concern. The pressure on inflation is keeping the Bank of England on its toes; we saw a 0.25% drop in early May, another in early August and the most recent in December, down to 3.75%. The likelihood of another fall seems less, because of underlying inflation.

UK GDP- The economy is not firing up, so further base rate falls are likely, but inflation still lurks in the shadows. Recent data shows that the economy is just about ‘alive’ but teetering on the edge of recession.

As always, please do not assume stock availability - check with the sales office!

Our reputation relies on word of mouth and testimonials from our valued customers, and as such we'd love for you to share reviews of your experiences with us on either Google, Facebook or TrustPilot if you have the time.

Thank you very much for your ongoing support of FORT!

Best regards,

Matt, Tim & Keith

The Directors